Not all Gold Glitters: A Critique of the Element and the Myths Surrounding It

A detailed analysis of one of the most famous commodities and Peter Schiff's favourite element, diving deep into the most well known "hedge" against inflation

Part 1: The Shinest Element

Gold, a metal that has captivated humanity for centuries, is more than just a symbol of love and wealth. It is a physical manifestation of human desire and the embodiment of our collective aspirations.

Throughout history, gold has played a central role in human society, from the earliest forms of currency to the most advanced technologies of today. Its malleability and beauty have made it a universal standard of value, a medium of exchange that transcends borders and cultures.

But why did we start using gold as a form of currency? People understood back then that exchanging a goat for 10 apples wouldn’t really be scalable at a societal level. Thus, the bartering system was disposed of, and we switched to copper, silver and gold coins.

But gold is more than just a medium of exchange. It is also a symbol of stability and security, a tangible representation of the trust that underlies all economic transactions. This is the reason why gold has been used as a standard of value for centuries, and why it remains a powerful force in the global economy today.

The gold standard is a financial system that is rooted in the idea that gold is the ultimate measure of value. It is a way of saying that the good times were when our economy was based on gold. However, today we are going to try and tackle the concept of the gold standard and explain why it is still relevant in our modern world. Despite its enormous complexity, we will provide bite-sized information that will help you begin to understand what we're talking about.

This is a list of the most gold reserves (in tons, mind you) held by countries all over the world.

The use of commodities as a reserve currency is a perilous endeavour, fraught with uncertainty and volatility. Commodities are subject to the whims of the market and can be prone to booms and busts that can have devastating effects on the economy. Furthermore, when a country ties its currency to a commodity, it cedes control over its monetary policy to the forces of supply and demand for that commodity.

This is particularly true for gold, which is a commodity but not a reserve currency. If gold were to be used as a reserve currency, it would mean that the countries with the most gold would have disproportionate economic and political power in the global financial economy. This would not only create imbalances and instability in the financial economy, but it would also have a spillover effect on the real economy, where some countries would have more power than others. This is a risky proposition and underscores the importance of diversifying the reserve currency.

Part 2: A Hedge against Inflation

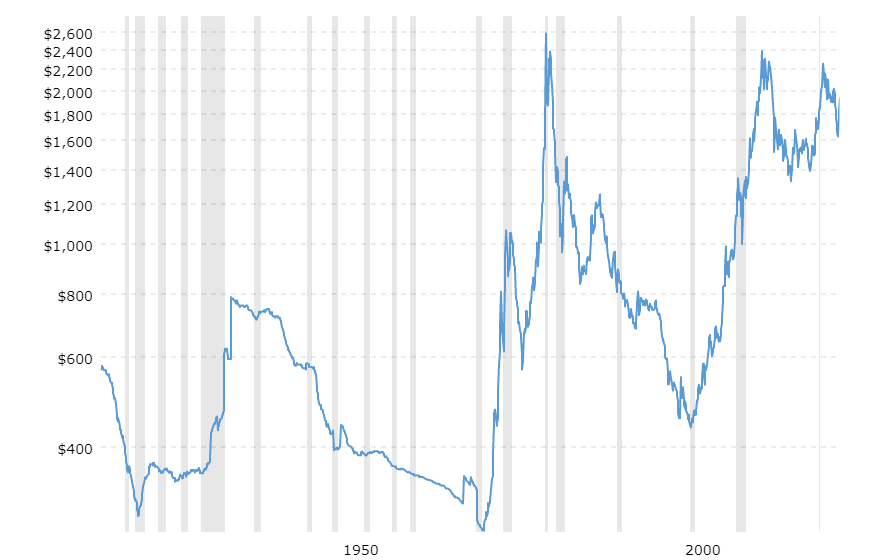

Gold has long been considered a bulwark against inflation, a safeguard for investors against the erosion of purchasing power. In this context, the nominal price of gold is often adjusted for the Consumer Price Index (CPI) to demonstrate its ability to preserve value over time. However, while gold may serve as an inflation hedge in the long term (for instance, over a period of 100 years from 1895 to 1999, the real value of gold remained practically unchanged), its effectiveness as an inflation hedge in the short- and medium-term is somewhat contentious.

Gold has long been touted as a hedge against inflation, a safeguard for investors against the erosion of purchasing power. However, short-term events such as the Tech Bubble burst, the 2008 Financial Crisis, and the 2020 Covid pandemic have brought into question the efficacy of gold as a hedge. The logistical nightmare of using gold as a reserve currency also adds to the scepticism. Most FX transactions around the world are cleared through clearing houses and settled in just one day, but imagine the challenges of conducting a cross-border transaction with gold, ensuring you have the reserves to pay for it, transporting the heavy metal, insuring it, and finding a safe enough space to store tons of it.

Ben Bernanke, the former Chair of the Federal Reserve of the United States, who led the organization during the Great Recession, also refutes the gold standard idea. He believes that the gold standard is just as inflation-prone and disarms a central bank's essential tools. Since the gold standard determines the money supply, there is not much scope for the central bank to use monetary policy to stabilize the economy. Under a gold standard, typically, the money supply goes up and interest rates go down in a period of strong economic activity - which is the reverse of what a central bank would normally do today.

Researchers at the world-renowned Chatham House, who were recently asked to consider a return to the gold standard, also agree that, while an effective hedge, gold's formal use is limited. Restrictions on money supply growth could provoke a severe downturn in the growth cycle of global economies. Gold can therefore have some utility in a portfolio of assets by spreading valuation risk, but it would not be very effective as a sole reserve asset.

Say what you want about Chairman Powell and that infamous meme of him spraying free money out of a gun. Say what you want about excessive borrowing, high Inflation, negative gearing and all the other byproducts of countries that print money to pay for the printers. One thing we should agree on is that gold, for all its fervour is not our answer.

We aim to be a contrarian's voice and will often voice opinions NOT held by many. We are only getting started laying into gold as there is too much to cover in one article. Up next on our list though, is Oil.

Therefore, we’ll end it with a quote from a popular tv show that fits the consensus on our economy:

“The system may be broken, but it built these roads”.

-Black Mirror

🗡️Thank you for reading our work and supporting our message🗡️